Ontario Wind: Worst value getting worser

A spreadsheet I regularly update with data on industrial wind turbine (IWT) generation in Ontario is cited in Parker Gallant's recent, Wind: worst value for Ontario consumers. The same post cites the Canadian Wind Energy Association (CanWEA) commentary on Ontario's recently released Long Term-Energy Plan 2017, which included:

Let's examine the "value" as electricity - as there is no market in Ontario for any subset of that commodity, including "affordable non-emitting".

Two definitions of "value" from the Oxford dictionary are pertinent:

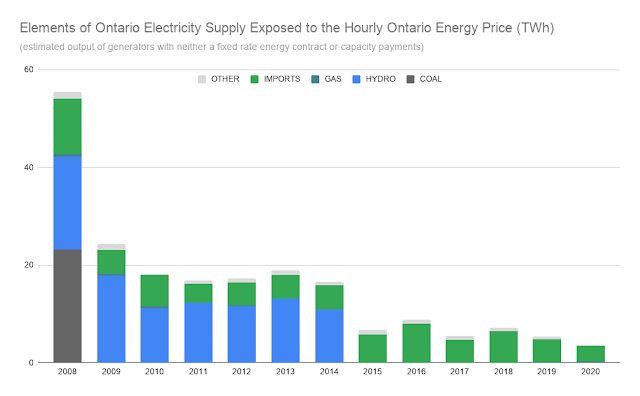

By the first definition wind is clearly the least valued generation type in Ontario. Using only very basic hourly data sets of Hourly summary totals of grid-connected (Tx) generation by type, valued at the Hourly Ontario Energy Price (HOEP), value factor can be calculated. A value factor above 1 means more valuable than average, below 1 means less valuable, and the lowest number consistently means wind.

This graphic is captured from a page I created to view summaries of basic IESO data sources:

While the picture with very basic system operator (IESO) doesn't seem to flatter wind, it actually does just that, mainly because wind is usually the first generator curtailed when there is excess supply, and therefore low prices. Adding my estimates of hourly distributed (Dx) generation and, particularly, curtailed generation shows wind's value factor down around 0.6 - meaning the market now values wind output 40% below the average value of generation.

That overview of market valuations show that CanWEA's value claims are, by the first definition from Oxford, simply wrong.

The second definition of value I cited relates the first definition, which I've demonstrated with market valuation, to the cost of the product.

I wrote this summer on information collected through a freedom of information request. That information ended in 2015 with the average cost paid for wind that year 49% above the average cost of supply.

![FOI+2[1]](https://morecoldair.files.wordpress.com/2017/11/foi21.png)

The period after 2015 is trickier to pin down, but the trend can be found by some publicly available IESO data. Monthly wind generation is part of the IESO's Generator Output by Fuel Type Monthly Report, and the IESO's Global Adjustments by Components includes that element of that charge due to wind generators. There is also a market price component which problematically means the numerator is low, and payments are also made to embedded (Dx) generators, so the denominator will also be low. There's many interesting issues with the publicly available data, but since we start in 2015 we see the combination provides a value not much higher than anticipated for that year. Summing up the monthly share of the global adjustment shown as due to wind, and dividing that by the sum reported output (Tx) for wind, reveals a steep 37.6% increase in the average cost of IWT output since 2015, to $192/MWh over the first 9 months of 2017:

I've added my estimates of distributed and, more significantly, curtailed wind, to this graphic. For 2015 the IESO reported 7.5% of (Tx) wind dispatched down; for 2016 they reported 19%, and my estimates are higher again for 2017 (near 25%).

It's wrong to claim, as CanWEA does, that the the combination of high, and still escalating costs couple with low commodity valuation make wind "the best value of consumers".

The opposite is true.

I'll finish with some detail on how my estimates, posted to my data site, should differ from IESO reporting.

Charting the IESO's reported monthly wind generation along with the monthly wind component of the global adjustment shows the two figures correlate less and less well over time.

Generally total costs don't drop as much as generation do in the summer months. This was known to be due to embedded generation and the fact wind is less productive in the summer months: the IESO does not pay embedded generators for the current month's output, but for prior months.

(aside: solar is a much larger distortion of monthly global adjustment costs for this reason)

However, the difference between the scale of generation declines and rate declines moving into the summer of 2017 is unprecedented. Between March and July the IESO's reported wind generation (Tx) dropped 68%, from 1,185 gigawatt-hours (GWh) to 378, but the monthly global adjustment charges dropped only 16% over the same months (from $158 million to $133 million).

Again the data can only make sense by looking beyond the available data summaries from the IESO. It appears that not only are distributed generation charges shifted from more productive months (for wind) to lesser productive ones, but that the curtailment that was particularly large during the spring (freshet) period in 2017 also pushed costs into the summer.

This combination meant that in July the IESO showed a wind component of the $133 million global adjustment on only 378 GWh of generation - making the average $352/MWh!

Two months later, in September, generation was almost identical (374 GWh), but the wind component of the global adjustment was a much lower $49 million - an average of $130/MWh.

All of which is to say that just because wind curtailment was high in October, and IESO estimates show likely record rates (Class B) will come in October, one should not assume the full costs of October's wind's are in October. Much of the cost of October's wind will be pushed into future months.

New wind energy provides the best value for consumers to meet growing demand for affordable non-emitting electricity.

Let's examine the "value" as electricity - as there is no market in Ontario for any subset of that commodity, including "affordable non-emitting".

Two definitions of "value" from the Oxford dictionary are pertinent:

- "The regard that something is held to deserve; the importance, worth, or usefulness of something."

- "The worth of something compared to the price paid or asked for it."

By the first definition wind is clearly the least valued generation type in Ontario. Using only very basic hourly data sets of Hourly summary totals of grid-connected (Tx) generation by type, valued at the Hourly Ontario Energy Price (HOEP), value factor can be calculated. A value factor above 1 means more valuable than average, below 1 means less valuable, and the lowest number consistently means wind.

This graphic is captured from a page I created to view summaries of basic IESO data sources:

While the picture with very basic system operator (IESO) doesn't seem to flatter wind, it actually does just that, mainly because wind is usually the first generator curtailed when there is excess supply, and therefore low prices. Adding my estimates of hourly distributed (Dx) generation and, particularly, curtailed generation shows wind's value factor down around 0.6 - meaning the market now values wind output 40% below the average value of generation.

That overview of market valuations show that CanWEA's value claims are, by the first definition from Oxford, simply wrong.

The second definition of value I cited relates the first definition, which I've demonstrated with market valuation, to the cost of the product.

I wrote this summer on information collected through a freedom of information request. That information ended in 2015 with the average cost paid for wind that year 49% above the average cost of supply.

The period after 2015 is trickier to pin down, but the trend can be found by some publicly available IESO data. Monthly wind generation is part of the IESO's Generator Output by Fuel Type Monthly Report, and the IESO's Global Adjustments by Components includes that element of that charge due to wind generators. There is also a market price component which problematically means the numerator is low, and payments are also made to embedded (Dx) generators, so the denominator will also be low. There's many interesting issues with the publicly available data, but since we start in 2015 we see the combination provides a value not much higher than anticipated for that year. Summing up the monthly share of the global adjustment shown as due to wind, and dividing that by the sum reported output (Tx) for wind, reveals a steep 37.6% increase in the average cost of IWT output since 2015, to $192/MWh over the first 9 months of 2017:

I've added my estimates of distributed and, more significantly, curtailed wind, to this graphic. For 2015 the IESO reported 7.5% of (Tx) wind dispatched down; for 2016 they reported 19%, and my estimates are higher again for 2017 (near 25%).

It's wrong to claim, as CanWEA does, that the the combination of high, and still escalating costs couple with low commodity valuation make wind "the best value of consumers".

The opposite is true.

I'll finish with some detail on how my estimates, posted to my data site, should differ from IESO reporting.

Charting the IESO's reported monthly wind generation along with the monthly wind component of the global adjustment shows the two figures correlate less and less well over time.

Generally total costs don't drop as much as generation do in the summer months. This was known to be due to embedded generation and the fact wind is less productive in the summer months: the IESO does not pay embedded generators for the current month's output, but for prior months.

(aside: solar is a much larger distortion of monthly global adjustment costs for this reason)

However, the difference between the scale of generation declines and rate declines moving into the summer of 2017 is unprecedented. Between March and July the IESO's reported wind generation (Tx) dropped 68%, from 1,185 gigawatt-hours (GWh) to 378, but the monthly global adjustment charges dropped only 16% over the same months (from $158 million to $133 million).

Again the data can only make sense by looking beyond the available data summaries from the IESO. It appears that not only are distributed generation charges shifted from more productive months (for wind) to lesser productive ones, but that the curtailment that was particularly large during the spring (freshet) period in 2017 also pushed costs into the summer.

This combination meant that in July the IESO showed a wind component of the $133 million global adjustment on only 378 GWh of generation - making the average $352/MWh!

Two months later, in September, generation was almost identical (374 GWh), but the wind component of the global adjustment was a much lower $49 million - an average of $130/MWh.

All of which is to say that just because wind curtailment was high in October, and IESO estimates show likely record rates (Class B) will come in October, one should not assume the full costs of October's wind's are in October. Much of the cost of October's wind will be pushed into future months.

Comments

Post a Comment