OPG's 2017 results grate

Yesterday Ontario Power Generation released their 2017 Financial Results:

That must be considered a great number in the context of the income history at OPG as it's the highest they've ever accomplished. The apparently excellent results may leave some wondering what critics commenting on the sector have been braying on about. I, a critic, have reviewed the results and found some things to bray about.

The "Financial and Operational highlights" OPG's release of the 2017 results (see pg 6) show two areas of significant financial change from the previous year. Unfortunately they are obscure:

The most significant business segment income change came from "Service, Trading, and Other Non-Generation." From page 44 of the Management's Discussion and Analyses (MD&A) section of the report:

This sale doesn't benefit electricity ratepayers due to legal changes introduced by the Wynne government requiring proceed from asset sales go to elsewhere (the Trillium fund). If you are suspicious Finance Minister Sousa is playing games to make Ontario's balance sheet, you might view this asset sale unfavourably.

OPG's 2017 report shows nuclear with the biggest improvement in the financial results of actual generation segments. Income before interest and income taxes grew to $57 (million) from $4. It is in this segment the improvement in "Depreciation and amortization" mainly resides, with that expense shrinking by $494M. Put another way, if there were no changes in this expense the nuclear segment would have shown a very large loss. Here's the description of the change (MD&A pg 40):

This indicates there was a growth of even more - $516M - related to "regulatory account balances." Most of this growth is described as due to a decision from the regulator (OEB) on rates for 2017 almost delivered in December (but still not actually changing rates paid to OPG even now). OPG "recorded net revenue of approximately $465 million in relation to the June 1, 2017 to December 31, 2017 period resulting from the OEB’s [rate] decision." OPG's interpretation of the rate decision is they note on page 5 of the MD&A.

OPG expects to recover an additional $21.36 per megawatt-hour for their nuclear production in the second half of 2017. I estimate that generation at 21.61 TWh resulting in a total of $461 million to be recovered from future ratepayers - almost spot on the stated $465 million in the MD&A.

Ontario consumers should know this means it's a bill they'll have coming - although with the government pushing the cost down the road with the [un]Fair Hydro Plan it won't be a cost existing ratepayers will be paying anytime soon.

The average rate for OPG's nuclear output in 2017 will eventually be around $70/MWh. $70/MWh was the rate in 2016, but consumers only paid $59/WWh during 2017 because the regulator spent the entire year, and half of the year before, mulling over how to fairly SMOOTH RATES! Consequently rates will climb over $80/MWh should the regulate ever act, due to a rate-riders created by their very lengthy rate review period.

Regulated (owned) hydro provided the bulk of OPG's income - as it has since the government regulated all sites at fixed rates in 2014, after Parker Gallant and I pointed to losses at non-regulated sites in 2013 (for more on that see my commentary on OPG's 2014 results). The difference between pending hydro rates and current ones is much smaller than the changes hitting nuclear, resulting in differed costs, form the consumers' perspective, of $15 million.

Notable in the reporting is, "During 2017 and 2016, OPG lost 5.9 TWh and 4.7 TWh of hydroelectric generation due to SBG conditions, respectively." With 30.7 TWh generated this indicates 16% of potential hydroelectric generation was curtailed. OPG does get paid for this curtailment, again via a regulatory variance account - so again it's a cost for future ratepayers.

As with nuclear, OPG's 2017 hydro results indicate higher rates for OPG hydro are coming.

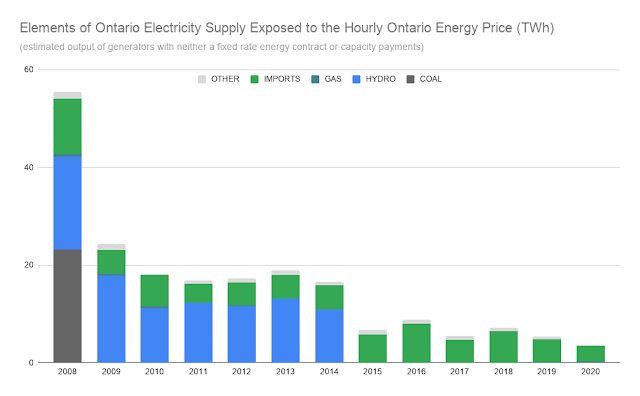

The report notes an "Enterprise Total Generating Cost per Megawatt-Hour" (TGC per MWh) of $50.66 for the year, up 4% from 2016 which is attributed to lower production at Darlington, "partially offset by higher SBG-adjusted hydroelectric electricity generation reflecting higher water flows." The TGC for nuclear was $70.95/MWh (what rates had been in 2016, and what they'll eventually average for 2017!). The TGC for hydro dropped to $23.79/MWh from $25.89, which OPG attributed to "higher water flows." The regulator, should they ever wrap up the 2017 rate application, might want to look over how to limit consumer costs in years of "high water flows," because despite 5.9 TWh of curtailment the actual output in 2017 was not much different than its been every year since 2009.

In summary, OPG reports, for 2017, $860 million of net income for the shareholder/province.

Which is great, but much of that, $490 million, is due to an expectation the regulator will allow recovery, from ratepayers, of costs calculated back to July 1, 2017. Much of the remainder is likely due to future recovery of costs for potential hydroelectric generation curtailed in 2017 - estimated at 5.9 TWh and $40 million/TWh, that would add another $236 million to future bills. Of the $860 million of profit OPG reports for 2017, over $700 million is essentially an IOU from future ratepayers.

Which is grating.

Ontario Power Generation Inc. (OPG or Company) today reported net income attributable to the Shareholder of $860 million for 2017, compared to $436 million in 2016.

That must be considered a great number in the context of the income history at OPG as it's the highest they've ever accomplished. The apparently excellent results may leave some wondering what critics commenting on the sector have been braying on about. I, a critic, have reviewed the results and found some things to bray about.

The "Financial and Operational highlights" OPG's release of the 2017 results (see pg 6) show two areas of significant financial change from the previous year. Unfortunately they are obscure:

- Depreciation and amortization ($578 million better)

- Other net (gains) expenses ($374 million better)

The most significant business segment income change came from "Service, Trading, and Other Non-Generation." From page 44 of the Management's Discussion and Analyses (MD&A) section of the report:

Segment earnings improved by $377 million in 2017 compared to 2016. The increase in earnings mainly reflected the gain on the sale of OPG’s head office premises and associated parking facility...

This sale doesn't benefit electricity ratepayers due to legal changes introduced by the Wynne government requiring proceed from asset sales go to elsewhere (the Trillium fund). If you are suspicious Finance Minister Sousa is playing games to make Ontario's balance sheet, you might view this asset sale unfavourably.

OPG's 2017 report shows nuclear with the biggest improvement in the financial results of actual generation segments. Income before interest and income taxes grew to $57 (million) from $4. It is in this segment the improvement in "Depreciation and amortization" mainly resides, with that expense shrinking by $494M. Put another way, if there were no changes in this expense the nuclear segment would have shown a very large loss. Here's the description of the change (MD&A pg 40):

Depreciation and amortization expenses, excluding amortization expense related to regulatory account balances, increased by $22 million, primarily due to new assets in service in 2017.

This indicates there was a growth of even more - $516M - related to "regulatory account balances." Most of this growth is described as due to a decision from the regulator (OEB) on rates for 2017 almost delivered in December (but still not actually changing rates paid to OPG even now). OPG "recorded net revenue of approximately $465 million in relation to the June 1, 2017 to December 31, 2017 period resulting from the OEB’s [rate] decision." OPG's interpretation of the rate decision is they note on page 5 of the MD&A.

OPG expects to recover an additional $21.36 per megawatt-hour for their nuclear production in the second half of 2017. I estimate that generation at 21.61 TWh resulting in a total of $461 million to be recovered from future ratepayers - almost spot on the stated $465 million in the MD&A.

Ontario consumers should know this means it's a bill they'll have coming - although with the government pushing the cost down the road with the [un]Fair Hydro Plan it won't be a cost existing ratepayers will be paying anytime soon.

The average rate for OPG's nuclear output in 2017 will eventually be around $70/MWh. $70/MWh was the rate in 2016, but consumers only paid $59/WWh during 2017 because the regulator spent the entire year, and half of the year before, mulling over how to fairly SMOOTH RATES! Consequently rates will climb over $80/MWh should the regulate ever act, due to a rate-riders created by their very lengthy rate review period.

Regulated (owned) hydro provided the bulk of OPG's income - as it has since the government regulated all sites at fixed rates in 2014, after Parker Gallant and I pointed to losses at non-regulated sites in 2013 (for more on that see my commentary on OPG's 2014 results). The difference between pending hydro rates and current ones is much smaller than the changes hitting nuclear, resulting in differed costs, form the consumers' perspective, of $15 million.

Notable in the reporting is, "During 2017 and 2016, OPG lost 5.9 TWh and 4.7 TWh of hydroelectric generation due to SBG conditions, respectively." With 30.7 TWh generated this indicates 16% of potential hydroelectric generation was curtailed. OPG does get paid for this curtailment, again via a regulatory variance account - so again it's a cost for future ratepayers.

As with nuclear, OPG's 2017 hydro results indicate higher rates for OPG hydro are coming.

The report notes an "Enterprise Total Generating Cost per Megawatt-Hour" (TGC per MWh) of $50.66 for the year, up 4% from 2016 which is attributed to lower production at Darlington, "partially offset by higher SBG-adjusted hydroelectric electricity generation reflecting higher water flows." The TGC for nuclear was $70.95/MWh (what rates had been in 2016, and what they'll eventually average for 2017!). The TGC for hydro dropped to $23.79/MWh from $25.89, which OPG attributed to "higher water flows." The regulator, should they ever wrap up the 2017 rate application, might want to look over how to limit consumer costs in years of "high water flows," because despite 5.9 TWh of curtailment the actual output in 2017 was not much different than its been every year since 2009.

In summary, OPG reports, for 2017, $860 million of net income for the shareholder/province.

Which is great, but much of that, $490 million, is due to an expectation the regulator will allow recovery, from ratepayers, of costs calculated back to July 1, 2017. Much of the remainder is likely due to future recovery of costs for potential hydroelectric generation curtailed in 2017 - estimated at 5.9 TWh and $40 million/TWh, that would add another $236 million to future bills. Of the $860 million of profit OPG reports for 2017, over $700 million is essentially an IOU from future ratepayers.

Which is grating.

Comments

Post a Comment