The magic of the phantom demand

The Ontario Energy Board's Market Surveillance Panel (MSP) released a report on December 19th which attracted some attention:

Some big numbers, but upon investigating I initially generated a thread on Twitter which concluded, "the impact of this mostly-grey money forensic investigation is an imperceptible lessening of the cost shift from class B to class A consumers." My position was supported when the system operator (IESO) responded to the MSP report:" IESO analysis shows a net market impact across all customer groups of less than $10 million."

And that's sort of the end of that hysteria, but since I looked I can't shake the feeling something is very wrong with the analysis - from the OEB report to the IESO response and the reporting on what occurred.

The MSP report connects exaggerating demand with price spikes. They need to explain that connection.

This is the technical explanation of how demand was inflated:

There is an IESO-controlled grid (ICG), which I usually describe as transmission-connected (Tx) consumption or generation. One consumer group on the ICG is local distribution companies (LDCs), within which there are also consumers and generators which are referred to in multiple ways including embedded and distributed (Dx). The issue discussed in the MSP report involved embedded consumers bidding into the capacity auction.

Embedded consumers have won 75% of the capacity awarded in the four auctions subsequent to the first auction, which is alleged to have triggered the error discussed in the MSP report.

So we're about $150 million into demand response capacity payments to embedded consumers (via aggregators who dominate the demand response auctions), and we've never activated the response.

Huh. How 'bout that?

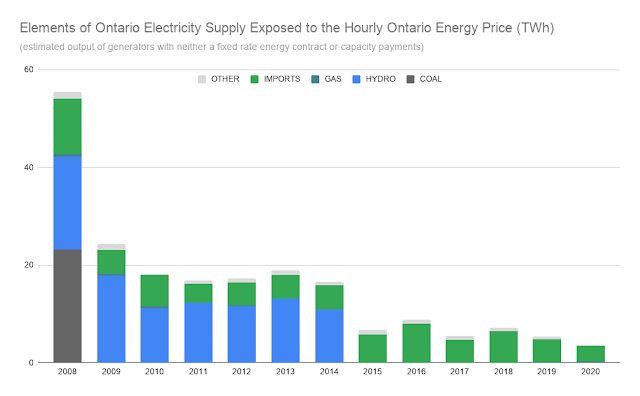

Supply from distributed generators is something the IESO reports on very little, relative to how often they contract it and fantasize about its role in the future. The number they report as "Ontario Demand" demonstrates how their operation was structured, with silos including direct wholesale consumers and LDCs comprising Energy/Ontario Demand along with generator consumption and (line) losses.

[caption id="attachment_6932" align="aligncenter" width="492"] from Table 3.3.3 tab of spreadsheet accompanying IESO reliability outlook[/caption]

from Table 3.3.3 tab of spreadsheet accompanying IESO reliability outlook[/caption]

Not included in the calculation, directly, is generation within the LDC networks. The IESO does include a monthly number for "Reported Embedded Generation (GWh)" in the workbook accompanying its reliability outlook (in Table 3.3.2), but the numbers are not known on an hourly basis.

Confused?

Me too - and perhaps also

the writers of the report. They claim two impacts of overestimating demand:

I think over-estimating demand should dull the Hourly Ontario Energy Price (HOEP) and lower the likelihood of price spikes. I respect the work of the Market Surveillance panel, but as far as I know overestimating demand would cause additional resources to be committed in the IESO's murky day ahead commitment process (DACP) which would drop the HOEP when excess supply must be adjusted to match supply in real time. I've queried the periods from May 17 to April 24 for not only the period in question, but all similar periods since 2010. While the HOEP was higher for the 2016-17 period in question than the same period in the prior, and subsequent, years, the cost of natural gas was too (particularly in the winter), and demand was higher too - so HOEP should be higher in the absence of any impact from the error.

A more meaningful comparison would be to see how the IESO HOEP (rate) compared to adjacent systems compared to how it usually does. It performed poorly - but it always does.

[caption id="attachment_6935" align="alignnone" width="672"] Graphic from IESO Monthly Market Report April 2017[/caption]

Graphic from IESO Monthly Market Report April 2017[/caption]

Somebody could try to quantify the degree of poorness, and the Market Surveillance Panel (MSP) does track those prices on a monthly basis in Table A-3 of their regular reporting. If they did they'd find that the period's increase in Ontario's HOEP was lower than the increase in the Michigan price zone (MISO) or the relevant New York price zones (NYISO). I don't see any evidence the changes in HOEP were out of character.

Price Spikes also occurred, but the connection here also escapes me: if too much supply is scheduled because additional demand is forecast it should follow that the possibility of price spikes should be lessened. Comparing the 11 months to the comparable periods in other years there is a jump in prices above $200 per megawatt-hour ($/MWh) in 2016-17, but upon examination the jump occurred due to low-demand hours experiencing price spikes. I suspect this is due to the IESO struggling to forecast two more general things: supply and demand.

Alastair Sharp's reporting on the MSP report indicated the demand response consumption was not the only embedded consumer/supplier change occurring at the time:

The timing is surprising, because by 2016 it would have been impossible to forecast hourly demand without forecasting embedded generation. Embedded generation reduces demand from the transmission-connected generators on the ICG - which is what the IESO reports as "Ontario Demand." The impact is clearer in pictures - on the left is what the IESO would need to schedule generators to meet, while on the right is the estimated actual consumption across the province. The addition of solar greatly distorted what the IESO considers "Ontario Demand" over the past decade.

[caption id="attachment_6937" align="alignnone" width="789"] Graphics were captured from Power BI report (6th tab)[/caption]

Graphics were captured from Power BI report (6th tab)[/caption]

The average hourly figures over two months display this, but realize some days have little solar, and some have an abundance. The point is that it's impossible to schedule the demand generators on the IESO-controlled grid will need to meet without forecasting embedded generators. This is a challenge the IESO was dealing with during the price spikes of 2016-17.

The highest HOEP of the period occurred in hour 20 of Saturday March 11th (7 - 8 pm), when demand response contracts wouldn't be relevant. The next highest, in hour 8 of April 12th, 2017 occurred when demand was a relatively paltry 15,591 MW. The issue - it seems to me - was no natural gas was online to provide flexibility: the IESO had curtailed overnight to find the flexibility for the morning ramp but something didn't work and the price spiked. This is similar to the hours noted in the MSP report, 20 and 21 on June 9th 2016: little flexible gas generation was operating in hour 19. It was a similar situation on hour 10 of April 6, 2017, the 5th highest HOEP spike: no flexible gas generators online. Not only was supply not tight on thees 4 days with price spikes, contracted supply was heavily curtailed for much of two of the them.

It's far more likely the price spikes on 2016-17 occurred due to limitations of the IESO's ability to forecast spasmodic generation (more politely known as variable renewable energy systems - or vRES), which is exactly what the MSP was attributing price spikes to during 2016 (without recognizing issues appearing as under-forecasting demand were more likely over-forecasts of embedded solar generation):

So those are my two problems with the two claims of higher HOEP and price spikes from over-forecasting demand due to an error integrating embedded demand "capacity resources": it's not only unlikely it did either, it obfuscates what we know is actually problematic.

if the report were correct, what would the impact be on consumer segment pricing?

If HOEP could be raised by $4.50 without impacting exports, one impact would be lower losses on exports - at least in terms of the global adjustment totals. Those would have been $88 million less if the rate was $4.50 higher, which would lower the global adjustment charges by $88 million.

Actual pricing for exports would not actually change. This is because there were significant congestion charges from May 2016 thru April 2017 (and beyond), adding about $8.75/MWh to the average price of exports. If the Ontario rate were lower presumable the price paid for congestion rents would have been higher. This would benefit Ontario ratepayers roughly equally as a (larger) credit would occur outside of the commodity price (in Wholesale Market Service Charges).

Class A and B consumers in Ontario would have seen opposite impacts if the HOEP had been $4.50/MWh lower. This is because more costs of supply would be recovered through the global adjustment mechanism which transfers costs from large Class A consumers to small Class B ones. Including an adjustment for exports receiving lower revenues at HOEP, I estimate Class A consumers would have paid $1.53/MWh more from May 2016-April 2017 ($42 million dollars in total), and Class B consumers $1.17/MWh less. If the IESO's claim that the total impact was approximately $225 million those figures would be reduced by about 60%. As the lower energy revenues would likely be accompanied by lower wholesale market service charges (due to higher congestion rents) it's likely the IESO would be nearer the truth in assessing the the total negative impact on consumers at around $10 million.

but...

I don't think the HOEP would be impacted from overestimating demand in the way the Ontario Energy Board's Market Surveillance Panel suggested.

"Over the 11- month period in question, the estimated impact on the HOEP and transmission loss uplift combined could have ranged as high as between $450 million to $560 million, although a simulation accounting for additional potential variables could yield lower estimates."

Some big numbers, but upon investigating I initially generated a thread on Twitter which concluded, "the impact of this mostly-grey money forensic investigation is an imperceptible lessening of the cost shift from class B to class A consumers." My position was supported when the system operator (IESO) responded to the MSP report:" IESO analysis shows a net market impact across all customer groups of less than $10 million."

And that's sort of the end of that hysteria, but since I looked I can't shake the feeling something is very wrong with the analysis - from the OEB report to the IESO response and the reporting on what occurred.

The MSP report connects exaggerating demand with price spikes. They need to explain that connection.

This is the technical explanation of how demand was inflated:

The unintended consequence began after the introduction of the first Demand Response (DR) auction in May 2016. At that time, the IESO’s scheduling algorithm had a mechanism to account for dispatchable loads – active participants in the wholesale market, capable of adjusting load in response to 5-minute prices – who may be consuming when not bidding into the market. However, the addition of DR resources that are embedded at the distribution level resulted in the IESO double-counting their demand in hours when they were not bidding: once as part of the IESO forecast generally and again by including them in a separate scheduling calculation akin to the mechanism applied to dispatchable loads.

There is an IESO-controlled grid (ICG), which I usually describe as transmission-connected (Tx) consumption or generation. One consumer group on the ICG is local distribution companies (LDCs), within which there are also consumers and generators which are referred to in multiple ways including embedded and distributed (Dx). The issue discussed in the MSP report involved embedded consumers bidding into the capacity auction.

Embedded consumers have won 75% of the capacity awarded in the four auctions subsequent to the first auction, which is alleged to have triggered the error discussed in the MSP report.

...as of July 2019, none of the hourly DR resources (embedded loads not directly connected to the IESO-controlled grid) – which account for the majority of DR capacity – have been activated.

So we're about $150 million into demand response capacity payments to embedded consumers (via aggregators who dominate the demand response auctions), and we've never activated the response.

Huh. How 'bout that?

Supply from distributed generators is something the IESO reports on very little, relative to how often they contract it and fantasize about its role in the future. The number they report as "Ontario Demand" demonstrates how their operation was structured, with silos including direct wholesale consumers and LDCs comprising Energy/Ontario Demand along with generator consumption and (line) losses.

[caption id="attachment_6932" align="aligncenter" width="492"]

from Table 3.3.3 tab of spreadsheet accompanying IESO reliability outlook[/caption]Not included in the calculation, directly, is generation within the LDC networks. The IESO does include a monthly number for "Reported Embedded Generation (GWh)" in the workbook accompanying its reliability outlook (in Table 3.3.2), but the numbers are not known on an hourly basis.

Confused?

Me too - and perhaps also

the writers of the report. They claim two impacts of overestimating demand:

- The estimated average increase in HOEP during the relevant period was as much as $4.50/MWh...

- ...the addition of fictitious demand often had a dramatic inflationary impact on the HOEP. To illustrate this impact, consider HE 20 on June 9, 2016. This hour had an HOEP of $1,619/MWh, the fourth highest in the history of the Ontario wholesale electricity market.

I think over-estimating demand should dull the Hourly Ontario Energy Price (HOEP) and lower the likelihood of price spikes. I respect the work of the Market Surveillance panel, but as far as I know overestimating demand would cause additional resources to be committed in the IESO's murky day ahead commitment process (DACP) which would drop the HOEP when excess supply must be adjusted to match supply in real time. I've queried the periods from May 17 to April 24 for not only the period in question, but all similar periods since 2010. While the HOEP was higher for the 2016-17 period in question than the same period in the prior, and subsequent, years, the cost of natural gas was too (particularly in the winter), and demand was higher too - so HOEP should be higher in the absence of any impact from the error.

A more meaningful comparison would be to see how the IESO HOEP (rate) compared to adjacent systems compared to how it usually does. It performed poorly - but it always does.

[caption id="attachment_6935" align="alignnone" width="672"]

Graphic from IESO Monthly Market Report April 2017[/caption]Somebody could try to quantify the degree of poorness, and the Market Surveillance Panel (MSP) does track those prices on a monthly basis in Table A-3 of their regular reporting. If they did they'd find that the period's increase in Ontario's HOEP was lower than the increase in the Michigan price zone (MISO) or the relevant New York price zones (NYISO). I don't see any evidence the changes in HOEP were out of character.

Price Spikes also occurred, but the connection here also escapes me: if too much supply is scheduled because additional demand is forecast it should follow that the possibility of price spikes should be lessened. Comparing the 11 months to the comparable periods in other years there is a jump in prices above $200 per megawatt-hour ($/MWh) in 2016-17, but upon examination the jump occurred due to low-demand hours experiencing price spikes. I suspect this is due to the IESO struggling to forecast two more general things: supply and demand.

Alastair Sharp's reporting on the MSP report indicated the demand response consumption was not the only embedded consumer/supplier change occurring at the time:

This involved the integration of small-scale embedded generation (largely made up of solar) into its wholesale model for the first time.

The timing is surprising, because by 2016 it would have been impossible to forecast hourly demand without forecasting embedded generation. Embedded generation reduces demand from the transmission-connected generators on the ICG - which is what the IESO reports as "Ontario Demand." The impact is clearer in pictures - on the left is what the IESO would need to schedule generators to meet, while on the right is the estimated actual consumption across the province. The addition of solar greatly distorted what the IESO considers "Ontario Demand" over the past decade.

[caption id="attachment_6937" align="alignnone" width="789"]

Graphics were captured from Power BI report (6th tab)[/caption]The average hourly figures over two months display this, but realize some days have little solar, and some have an abundance. The point is that it's impossible to schedule the demand generators on the IESO-controlled grid will need to meet without forecasting embedded generators. This is a challenge the IESO was dealing with during the price spikes of 2016-17.

The highest HOEP of the period occurred in hour 20 of Saturday March 11th (7 - 8 pm), when demand response contracts wouldn't be relevant. The next highest, in hour 8 of April 12th, 2017 occurred when demand was a relatively paltry 15,591 MW. The issue - it seems to me - was no natural gas was online to provide flexibility: the IESO had curtailed overnight to find the flexibility for the morning ramp but something didn't work and the price spiked. This is similar to the hours noted in the MSP report, 20 and 21 on June 9th 2016: little flexible gas generation was operating in hour 19. It was a similar situation on hour 10 of April 6, 2017, the 5th highest HOEP spike: no flexible gas generators online. Not only was supply not tight on thees 4 days with price spikes, contracted supply was heavily curtailed for much of two of the them.

It's far more likely the price spikes on 2016-17 occurred due to limitations of the IESO's ability to forecast spasmodic generation (more politely known as variable renewable energy systems - or vRES), which is exactly what the MSP was attributing price spikes to during 2016 (without recognizing issues appearing as under-forecasting demand were more likely over-forecasts of embedded solar generation):

The High HOEPs were primarily caused by under-forecasts of demand and short-notice losses of supply (curtailing of imports and under-generation of wind facilities relative to their forecast production).

So those are my two problems with the two claims of higher HOEP and price spikes from over-forecasting demand due to an error integrating embedded demand "capacity resources": it's not only unlikely it did either, it obfuscates what we know is actually problematic.

if the report were correct, what would the impact be on consumer segment pricing?

If HOEP could be raised by $4.50 without impacting exports, one impact would be lower losses on exports - at least in terms of the global adjustment totals. Those would have been $88 million less if the rate was $4.50 higher, which would lower the global adjustment charges by $88 million.

Actual pricing for exports would not actually change. This is because there were significant congestion charges from May 2016 thru April 2017 (and beyond), adding about $8.75/MWh to the average price of exports. If the Ontario rate were lower presumable the price paid for congestion rents would have been higher. This would benefit Ontario ratepayers roughly equally as a (larger) credit would occur outside of the commodity price (in Wholesale Market Service Charges).

Class A and B consumers in Ontario would have seen opposite impacts if the HOEP had been $4.50/MWh lower. This is because more costs of supply would be recovered through the global adjustment mechanism which transfers costs from large Class A consumers to small Class B ones. Including an adjustment for exports receiving lower revenues at HOEP, I estimate Class A consumers would have paid $1.53/MWh more from May 2016-April 2017 ($42 million dollars in total), and Class B consumers $1.17/MWh less. If the IESO's claim that the total impact was approximately $225 million those figures would be reduced by about 60%. As the lower energy revenues would likely be accompanied by lower wholesale market service charges (due to higher congestion rents) it's likely the IESO would be nearer the truth in assessing the the total negative impact on consumers at around $10 million.

but...

I don't think the HOEP would be impacted from overestimating demand in the way the Ontario Energy Board's Market Surveillance Panel suggested.

I am told I did not get this quite right. The fictitious/phantom demand was not included in the day-ahead commitment process, so resources were not scheduled to meet it.

ReplyDeleteThat would spike HOEP as resources became suddenly insufficient to meet suddenly higher demand.